Customer Lifetime Value (CLTV) – Calculate the code correctly

The calculation of the Customer Lifetime Value (CLTV) is worthwhile because this indicator has a high potential for success. It is therefore also worthwhile to put the CLTV calculation at the centre of e-commerce management. In this article, I show how to calculate customer lifetime value, how the database is determined and which management potentials result from customer lifetime value.

Do you need support with customer loyalty and the determination of the customer lifetime value for your online shop? Then use the short line to Prof. Richard Geibel: Tel. 0221 973 199 722, mail: info@ecommerceinstitut.de.

Contents

- Definition of Customer Lifetime Value

- Customer Lifetime Value (CLTV) calculation – the formula

- Sample calculation

- Data sources for the CLTV in practice

- Segmentation as a solution

- Calculation challenges

- Corporate management with the CLTV

- Conclusion

Customer Lifetime Value (CLTV) calculation – the definition

The Customer Lifetime Value is the net contribution margin generated by purchases made by a single customer during a given period, the Customer Lifetime. The Customer Lifetime Value model envisages that a customer is bound to a company for a longer period of time after an acquisition and purchases goods or services from that company. The basis for the customer lifetime value model is, therefore, the loyalty of the customer. The customer lifetime value calculation compares the present value of the net contribution margins of a customer with the costs of the initial acquisition.

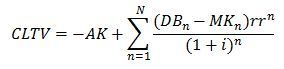

Customer Lifetime Value (CLTV) calculation – the formula

The following equation can be used to calculate the Customer Lifetime Value:

Where:

- AK (Akquisitionkosten): acquisition costs for the individual customer

- DB (Deckungsbeitrag I): contribution margin I

- MK ( Marketing und Kundenbetreuungskosten): marketing and customer support costs

- RR (Retentionrate): retention rate or repurchase rate

- i: discount rate

- n: period under consideration

- N: the total number of periods used

- CLTV: Customer Lifetime Value

Customer Lifetime Value calculation – an example

For the example of Customer Lifetime Value in e-commerce, let us assume that a customer usually spends € 200 per year at a company, resulting in a contribution margin I of € 80. The one-time acquisition costs are € 50, the annual direct costs for customer care, etc. are € 10, and the retention rate is 85%. The customer loyalty period is assumed to be 5 years and the interest rate is 5%.

According to the formula, this results in the customer lifetime value calculation:

CLTV = – 50 € + 194.07 € = 144.07 €

It becomes clear that due to high acquisition costs, limited customer loyalty, but also the discounting of the customer lifetime value as a present value, a significant number of negative factors are involved. However, the merit of the CLV model is that it provides an objective indicator for these factors and for determining the present value of the customer relationship. This present value is particularly important for determining the budget for customer acquisition.

Customer Lifetime Value calculation – the practice

Since the Customer Lifetime Value is a composite indicator, the determination is relatively complex. At the same time, the customer lifetime value is oriented towards the future and therefore mainly contains target figures. Finally, different data sources are required, which must provide consistent data.

The data sources for the Customer Lifetime Value

The customer lifetime value includes data from several sources that need to be merged. First of all, controlling and accounting provide data on the contribution margin and the discount factor. Information on the retention rate and on marketing and customer loyalty costs comes from the CRM, while online marketing can make statements about the online acquisition costs.

Since all data are planning data, individual planning must be coordinated. The assumptions about exogenous factors of the planning have to be synchronized, also endogenous planning parameters have to be coordinated. Since planning is usually based on historical values, the individual data sources must be able to access the respective historical values.

Aggregated or individual data

A question of complexity and the capacity needed to manage complexity is the question of aggregating data. The customer lifetime value can be determined individually, i.e. for individual customers, or – in the sense of a simplified flat rate – via aggregates. Aggregates – e.g. the “average male customer” – have the advantage that they can be determined much more easily, but aggregation inevitably means loss of information.

On the other hand, individual data makes it possible to continuously check and adjust the underlying model for the Customer Lifetime Value. With the help of individually collected data, aggregations can also be carried out more easily. However, the collection of individual CLTV data is very time-consuming and requires the consent of the customers in a special way.

Customer Lifetime Value calculation – segmentation as a compromise

Because of the difficulties with either highly aggregated or individual data – as is often the case – segmentation is the ideal solution. In segmentation, customers with identical and typical characteristics are combined into segments, for which the customer lifetime value is then calculated.

Segments can be defined according to demographic characteristics such as age, gender, place of residence or educational status. But online channels or the use of different devices can also shape the definition of segments. Finally, situational segments can also be used if, for example, campaigns and actions are carried out that are intended to support customer loyalty.

Customer Lifetime Value calculation – challenges in the calculation

The calculation of the customer lifetime value is based on a number of model hypotheses that make collecting the key figure a challenge for data analysts. Above all, the general indicators of acquisition costs, retention rate, discount rate, but also the underlying length of customer loyalty are difficult.

Determination of acquisition costs

The customer lifetime value model is based on the assumption that no further acquisition costs arise after the initial acquisition of a customer. However, the fact that regular customers can also use channels that can lead to direct marketing expenses is ignored. If the Customer Lifetime Value is granular, ie. should be determined for individual customer segments, these subsequent acquisition costs must be taken into account.

Typical acquisition costs are click costs on Google Adwords. In order to determine the effective acquisition costs, the cost-per-order or cost-per-acquisition can be determined using a simple formula. To do this, you need an average click cost rate, the CPC, and the average conversion rate. This results in the value for the acquisition costs:

CPO = CPC / CR

An example makes the connection clear. With an average CPC of 0.75 euros and a conversion rate of 3%, this results in a CPO of 25 euros. The example makes it clear that the acquisition costs in online marketing can be considerable even with moderately positive costs.

Determination of the retention rate

Defining a retention rate for the entire duration of the customer relationship is also problematic. It would be more realistic to consider a dynamic course of the retention rate. It should be plausible that the probability of repurchase decreases over time. Certainly, it should also be decisive whether the company’s product range consists of durable goods or consumer goods.

Determination of the discount factor

The discount rate also has a notable influence on the level of the customer lifetime value, but can only be determined with the help of forecasts. The interest rate should reflect the cost of capital and the risk that the customer will jump off. Then the acquisition costs cannot be amortized and have to be written off.

Determination of the customer loyalty period

The customer retention period significantly determines the customer lifetime value. When determining this number, the company depends on having valid past values that enable the determination of an average customer retention period. However, if customer loyalty measures are intensified, which also extend customer loyalty, the overall model could appear less reliable.

Customer lifetime value calculation – corporate management with the CLTV

Despite all the difficulties that arise when determining the customer lifetime value, the model is well suited to implementing profit-oriented corporate management.

The main contribution of the Customer Lifetime Value model to earnings control lies in the segmentation of customer groups. If one differentiates customer groups according to the expected CLTV, online marketing measures and investments can be carried out more efficiently. A tried and tested approach is to group the customer segments in an ABC distribution. This is similar to the Pareto principle, also known as the 80/20 rule: 20% of customers account for 80% of the contribution margins.

It is also obvious to intensify customer loyalty measures for customers with high CLTV. The effect of discounts and other promotions on the contribution margins can also be determined with the help of the customer lifetime value. After all, the model is an important basis for allocating the budget for customer service and customer loyalty measures.

Conclusion

Even if the model of customer lifetime value is somewhat complex, it can be used in many ways and provides important insights that should not be dispensed within online marketing and e-commerce. If you also consider that the customer lifetime value is the central indicator at Amazon – especially with prime customers – it becomes clear that for many e-commerce companies, from a strategic and cultural perspective, a discussion of the customer lifetime value is useful and necessary.

Literature: Jeffery, Mark: Data Driven Marketing. The 15 Metrics everyone in Marketing should know, Hoboken 2010, p. 134 ff.